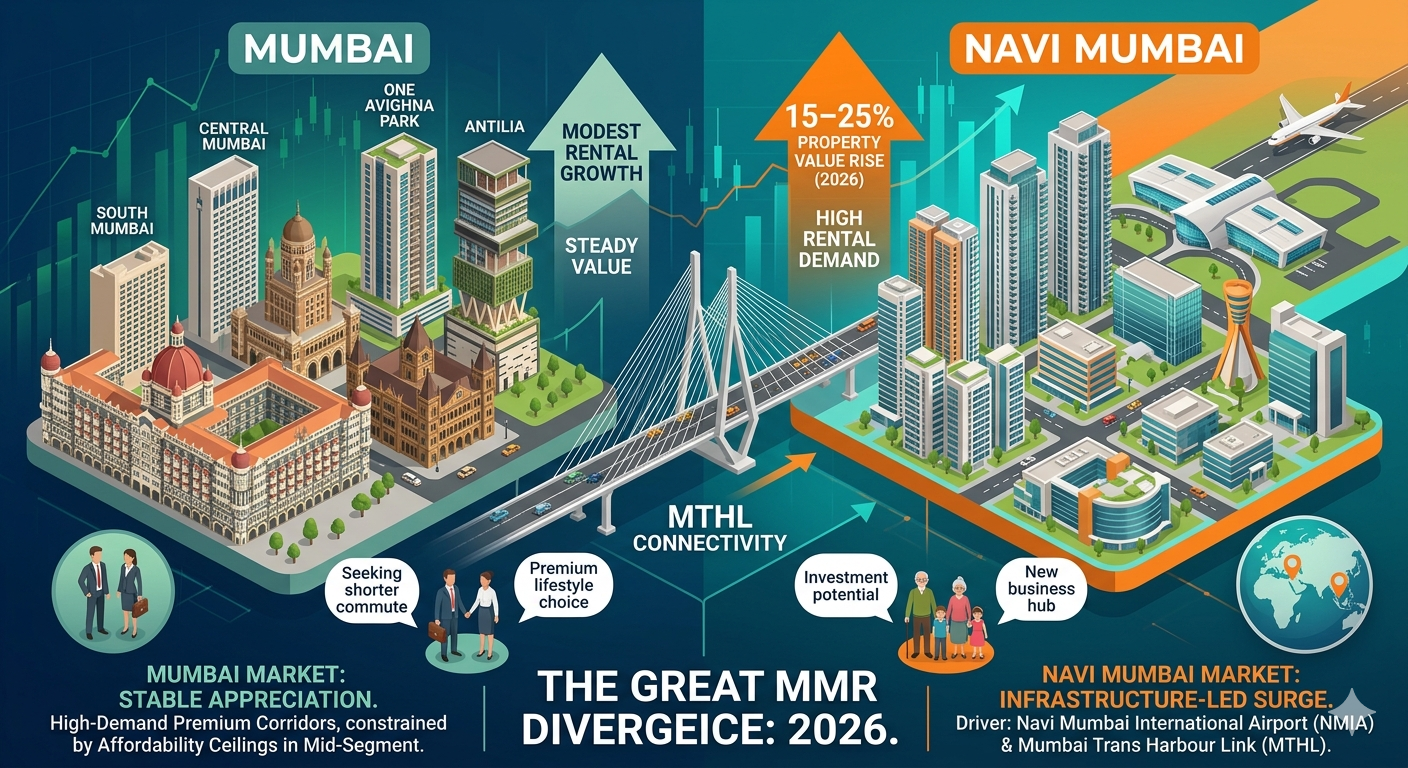

For years, Mumbai and Navi Mumbai were spoken of in the same breath — twin pillars of the Mumbai Metropolitan Region (MMR), each complementing the other. But a close look at rental trends in 2026 tells a strikingly different story: the two markets are drifting apart.

Driven by diverging demand patterns, a burst of infrastructure completions, and a tenant base that is making increasingly deliberate choices about where to live, these two cities now offer fundamentally different value propositions to renters and investors alike.

Navi Mumbai: No Longer a "Future Market"

The phrase that keeps appearing in broker conversations across Kharghar, Panvel, and Ulwe in 2026 is a telling one: Navi Mumbai is no longer speculative — it is structural.

For a long time, the city's appeal rested on promises: an airport that was always two years away, metro lines under construction, connectivity that was good but not great. In 2026, those promises have materialised. The Mumbai Trans Harbour Link (MTHL) now cuts travel between Sewri and Nhava Sheva to under 20 minutes, effectively collapsing what was once a deterrent commute for professionals working in South Mumbai or BKC. The Navi Mumbai International Airport is operational, and its gravitational pull on the surrounding rental market — particularly in Ulwe, Dronagiri, and Panvel — is no longer theoretical.

Rental yields across major nodes in Navi Mumbai are averaging 5–6%, with select pockets performing higher. Ulwe and Panvel are consistently cited as the strongest combinations of rental income and long-term capital appreciation. Vashi, despite an 8.86% dip in per-square-foot rental rates in some data cuts, remains the most premium node, commanding an average asking price of over ₹28,000 per sq ft for purchase.

Rental demand is especially strong near employment zones, educational institutions, and transport nodes. Professionals, hybrid workers, and young families are all moving in, and — critically — many renters are converting to buyers as EMI costs and monthly rents begin to converge, reinforcing demand fundamentals for years ahead.

Mumbai: Premium Is Firm, Mid-Segment Is Squeezed

Mumbai's rental market is not struggling — at the top, it is thriving. South Mumbai and South-Central corridors command ₹45,000–75,000 per sq ft for 2BHK purchases, and rentals in Bandra, Juhu, and Worli remain out of reach for all but the most well-paid tenants. Demand from senior executives, expatriates, and BFSI professionals keeps occupancy high in well-located premium inventory, and vacancy risk in quality Grade A residential developments remains low.

The Commercial Boom

The commercial side tells an even stronger story. Mumbai recorded a record 6.6 million sq ft of gross office leasing in Q1 2026 alone — its strongest quarter in years. BFSI firms led with a 44% share, followed by IT and engineering companies, and Global Capability Centres accounted for over 30% of leasing. With Grade A office vacancy tightening to 9.2% and no major new supply additions, office rentals continued to firm up across BKC, Lower Parel, and Powai. Mumbai's CBD posted a 13.7% three-year compound annual growth rate in office rents, the highest of any commercial district in India.

The Residential Squeeze

But the residential mid-segment tells a harder story. Mumbai recorded a record 19,775 residential unit launches in Q1 2026 — up 25% quarter-on-quarter — suggesting developers are responding to demand. Yet the median purchase price per square foot across key areas sits around ₹27,500 and above, and rental yields in the city remain modest at roughly 3.84%, well below the national average of 5.09% and well below what Navi Mumbai is delivering.

For a tenant doing the arithmetic on a 2BHK — comparing a ₹60,000-per-month flat in Andheri against a ₹43,000 flat in Kharghar with a 25-minute MTHL commute — Mumbai is increasingly a harder sell.

The Tenant Who Is Choosing Differently

The divergence is ultimately a story about a tenant whose calculus has changed.

A few years ago, tolerating a cramped flat in a Mumbai suburb was the accepted trade-off for proximity to work, nightlife, and urban infrastructure. In 2026, that trade-off has eroded. Navi Mumbai now has the malls, the schools, the hospitals, the metro connections, and the green spaces. It also has the airport. What it doesn't have is Mumbai's price tag — and for a growing share of the MMR's working population, that is the deciding factor.

Families in particular are driving this shift. A gated-community 2BHK in Kharghar or Nerul, with a clubhouse, school nearby, and metro access, starting at ₹18,000–25,000 per month, offers a quality-of-life proposition that inner Mumbai simply cannot replicate at equivalent cost. Young professionals and hybrid workers — no longer tethered to a five-day office commute — are arriving at similar conclusions.

The numbers confirm what brokers have been observing on the ground: Navi Mumbai accounted for 34% of total MMR residential sales through 2025, the largest share of any zone in the region. In Q1 2026, it contributed 17% of new residential launches — second only to Mumbai's Western Suburbs. This is not a niche trend. It is a structural realignment of where MMR residents choose to live.

What to Watch: Micro-Market Nuances

Not every node within Navi Mumbai is riding the same wave. Airoli saw a steep 32% drop in rental rates per square foot in recent data, a reminder that supply-demand dynamics vary sharply by micro-market. Newer nodes like Taloja and parts of Ulwe have seen a surge in affordable new supply — units priced between ₹5,000–10,000 per sq ft — which can compress yields for investors who didn't enter early.

The consensus among market observers is that appreciation will continue at 10–20% annually through 2027, but the sharpest gains will be concentrated in airport-adjacent corridors and established nodes with strong tenant pipelines.

In Mumbai, the constraint is different: it is supply, not demand. With new launches at record levels but land availability structurally limited, the city's rental market will be shaped less by new inventory and more by redevelopment timelines, infrastructure access, and the premium that tenants are willing to pay for an address that Navi Mumbai, however good it gets, still cannot replicate.

The Bottom Line

Mumbai and Navi Mumbai in 2026 are not a winner and a loser. They are two distinct markets, each making a coherent case for itself to a different kind of renter.

Mumbai retains its hold on premium demand, commercial gravity, and the irreplaceable prestige of India's financial capital. Its office market is booming, its luxury residential segment is firm, and BKC remains one of the country's most valuable business addresses.

But for the vast middle of the MMR rental market — the families, the value-conscious professional, the hybrid worker recalculating their commute — Navi Mumbai in 2026 is not a compromise. As infrastructure investment continues to close the gap in lifestyle and connectivity, that divergence is unlikely to reverse. If anything, it is just getting started.

Data sourced from Cushman & Wakefield MarketBeat Q1 2026, Square Yards, NoBroker, Global Property Guide, and broker intelligence across MMR as of mid-2026.

Key Takeaways for Investors & Tenants in 2026

- Navi Mumbai yields (5–6%) are significantly outperforming Mumbai's residential average (3.84%).

- The MTHL and NMIA have transformed Navi Mumbai from a speculative "future market" into a structural reality.

- Mumbai's commercial sector is booming (6.6M sq ft leased in Q1 2026), but its mid-segment residential is squeezed by high ticket sizes.

- Tenant calculus has shifted: Quality of life and space in Navi Mumbai are winning over traditional Mumbai proximity.

- Micro-market selection is critical: Airoli faces supply-led yield compression, while airport-adjacent corridors continue to see sharp appreciation.

— Dr. Avinash Jagdale

Managing Director, JPrime Group